Students can read the important questions given below for Production and Costs Class 12 Economics. All Production and Costs Class 12 Notes and questions with solutions have been prepared based on the latest syllabus and examination guidelines issued by CBSE, NCERT and KVS. You should read all notes provided by us and Class 12 Economics Important Questions provided for all chapters to get better marks in examinations. Economics Question Bank Class 12 is available on our website for free download in PDF.

Important Questions of Production and Costs Class 12

MCQs

Question. In the short run TPP changes with the change in which of the following factors

a) Economic cost

b) Fixed factors

c) All the factors

d) Variable factors

Answer

D

Question. The general shape of TPP in the short run is

a) Inverse U shaped

b) U shaped

c) Hyperbola

d) V- shaped

Answer

A

Very Short Answer Type Questions

Question. What is meant by production?

Answer : Production means transformation of input into output through specific process.

Question. When there are diminishing returns to a factor, total product always decreases.

Answer : False, as TPP increases at a decreasing rate when there is diminishing returns to a factor.

Question. Increase in TPP always indicates that there are increasing returns to a factor.

Answer : False, TPP increases even when there are diminishing returns to a factor.

Question. Calculate MP for the following.

Answer : MP: 0 5 8 10 5 0 -4

Question. Why AVC and AFC always lie below AC?

Answer : AC is the summation of AVC & AFC so AC always lies above AVC & AFC.

Question. When TVC is zero at zero level of output, what happens to TFC or Why TFC is not zero at zero level of output?

Answer : Fixed cost are to be incurred even at zero level of output.

Short Answer Type Questions

Question. What is change in quantity demanded?

Answer : It is also called movement along a demand curve. Due to change in its own price, quantity of commodity changes.

There are two type of change in quantity of Demand

(a) Extension in Demand

(b) Contraction in Demand

Question. Define cost concept. What are the different types of costs?

Answer : The expenditure incurred on various inputs is known as the cost of production.

Types of Cost

1. Money Cost: – Total money expenses by a firm for producing a commodity.

2. Explicit Cost and Implicit Cost: – Actual payment made to outsiders is Explicit Cost.

Cost of self-supplied factors in implicit cost.

3. Real Cost: – All the pain, sacrifices, discomforts involved in producing factor services to produce commodity.

4. Opportunity Cost: – It is the cost of next best alternative foregone.

5. Short Run Cost:-

I. Fixed Cost: – Cost of fixed factors.

II. Variable Cost: – Cost of variable factors

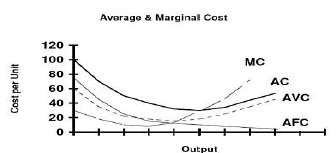

Relationship between AC, MC & AVC

Long Answer Type Questions

Question. Explain the relation between Marginal Cost and Average Variable Cost with the help of diagram.

Answer : Relationship holding between marginal cost and average variable cost is also one of the many cost relationships. When marginal cost is less than average variable cost, average variable cost is decreasing. On the contrary, when marginal cost is greater than average variable cost, average variable cost is increasing. In some cases, this also means that

average variable cost takes on a U-shape, though this is not guaranteed since neither average variable cost nor marginal cost contain a fixed cost component. In business, both the fixed and variable costs are used to determine the cost of production. Marginal costs measure the change in production expenses for making each additional item. Variable costs

reflect the materials necessary to manufacture or make each product. As a result, the variable costs directly impact the marginal cost.

Let’s take an example, Mary own a bakery and she is considering adding other options to her existing menu along with cakes. Other new stuffs will be sandwiches. But she will need to look at both the variable and marginal costs to determine if it’s worth it. She should calculate the average cost of the extra ingredients and labour necessary to make the sandwiches.

Then, she will need to use the variable costs and fixed costs to calculate the marginal cost. If the marginal cost associated with a sandwich is too high to bring in profit, the she wouldn’t want to bother adding it.

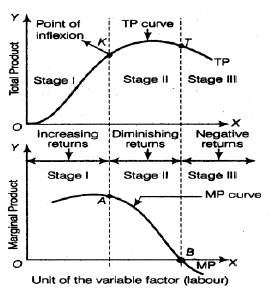

Question. State the behaviour of Marginal product is the Law of Variable Proportions. Explain the causes of this behaviour.

Answer : Law of variable proportion states that the marginal product of the factor input, initially rises with the employment level. But soon it starts falling once it reaches to a certain level of employment.

This law can be well understood from the below diagram:

From the above diagram and table, we can jot down observation below:

(iv) When marginal product is negative, total products starts declining Law of variable proportion basically depends on diminishing returns to marginal factor and the causes are imperfect factor sustainability, poor coordination between the factors, etc.